WLE-supported research is addressing the increasing demand for affordable, pro-poor flood insurance products that protect farmer assets and strengthen resilience.

Background

Faced with the escalating threat of more frequent and destructive flooding, vulnerable farmers and governments are increasingly recognizing the potential of flood insurance products. In India, for instance, a national crop insurance scheme (Pradhan Mantri Fasal Bima Yojana) was launched in February 2016 with the aim of reaching 61.2 million vulnerable farmers by 2019–2020. But this, and other similar schemes, have encountered several challenges: the data they rely upon is limited; they often fail to reach the poorest farmers – particularly women, youth or farmers from other disadvantaged groups; and payouts tend to be delayed because of inefficiencies and difficulties verifying losses.

Innovation

A close examination of these deficiencies and experience gained through several WLE-supported projects in Bangladesh, India and Sri Lanka has helped inform the development of innovative pro-poor insurance products. One is an index-based flood insurance scheme that uses flood modelling data to estimate flood depths and duration and satellite data to help assess flood damage. The approach removes the need to verify claims via field visits, speeds up the delivery of compensation from insurers and helps ensure that premiums remain affordable. Compensation is triggered automatically when floods reach a certain threshold; the exact amount determined by the duration and depth of a flood.

The second innovation is a bundled insurance product that provides compensation alongside improved drought tolerant wheat or flood-resistant rice seed varieties, agricultural inputs such as fertilizers and information on appropriate agronomic practices. An early warning system is also built in: weather forecasts in local languages are sent via SMS so that farmers can take necessary precautions to protect their crops and other assets. In this clustered approach insurance is just one component of a wider resilience strategy tailored to climate-vulnerable farmers.

Partnerships with organizations and initiatives working directly with farmers – including microfinance lenders in Bangladesh and start-ups in India – have encouraged uptake. Insurance companies have been attracted to the potentially large portfolios they can access through these partnerships, the distributed risk in coverage areas and the focus on strengthening farmer resilience. Farmers benefit from relatively modest premiums of US$6-9 per season, depending on the level of risk.

Impact

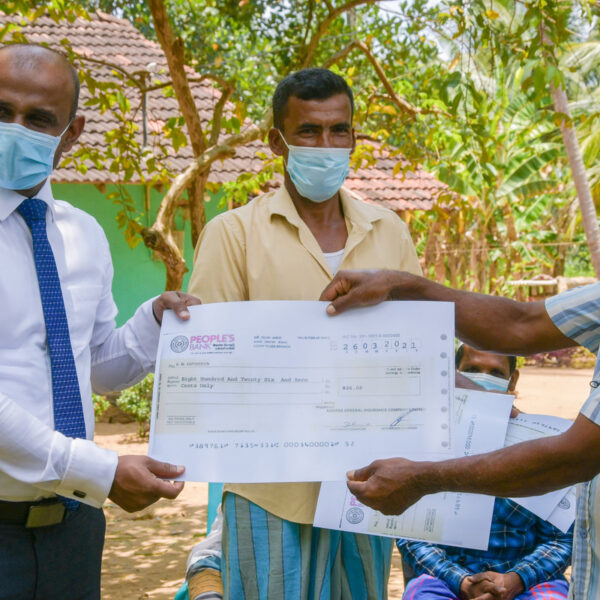

Some 9,300 farmers across Bangladesh, India and Sri Lanka had received insurance payouts totaling US$150,000 by 2021. These payouts have proved that the concepts are viable, and governments in South Asia and Southern Africa are now looking closely at the model to improve their own schemes and extend coverage to more farmers.

Challenges

Gathering data on loss and damage, particularly at the household level, remains a significant challenge, and without more granular data at the village level, insurance companies may be tempted to charge higher premiums. Moreover, there is a critical need to share data across institutions, regions and countries to better anticipate flood risks, for example in downstream locations which may not have experienced extreme rainfall. There is a further need for multi-institutional coordination and cooperation between agencies to more effectively manage financial risks in the context of disaster risk management.

There is also an awareness gap: flood insurance schemes are still not well known and many farmers have a limited understanding of how insurance products work. Capacity strengthening should therefore also include financial literacy alongside other measures such as implementing climate-smart agronomic practices. For farmers that remain resistant to taking out flood insurance the participatory approach adopted by WLE and its partners could help – this involved researchers working closely with farmers to build trust and demonstrate risks via simulations.

Next steps

Researchers are now seeking to apply their experience in other flood-prone regions such as Southern and Eastern Africa where they are exploring potential partnerships with African Risk Capacity and regional insurance companies. They are also considering insurance products that cover multiple climate-related threats – not just floods but also heatwaves, droughts and extended cold spells.